Our Thesis on STX

We rarely write about one particular token, but given the volume of requests for our thesis on STX, especially after the recent announcement, we are consolidating thoughts here in one place. Hope this is helpful to those seeking to understand the STX ecosystem and the reasons behind our conviction.

Disclaimer: My firm (obviously) owns STX. This is not financial advice—only an investment thesis.

Most who know me for calling the BTC thesis early know that STX is my highest-conviction pick on the secondary market, and here is a consolidated list of why:

OG Blue-chip Crypto Project: Stacks was founded in 2013 by Muneeb Ali, a PhD in Computer Science at Princeton University at the time, and Ryan Shea. Stacks is YC class of 2014 with subsequent backers (while private) including Union Square Ventures, Lux Capital, and more.

The First Compliant Token: A key driver for institutional adoption is to use STX as the de facto BTC staking provider.

STX was the first SEC-compliant token issuance and, in 2021, released its decentralization framework (also filed with updates to the SEC as a non-security). While many other major tokens will still undergo the battle with the SEC to fight off the "security token" label, STX has achieved sufficient decentralization like Ethereum did in 2017 and will not have to be distracted by legal fights going forward.

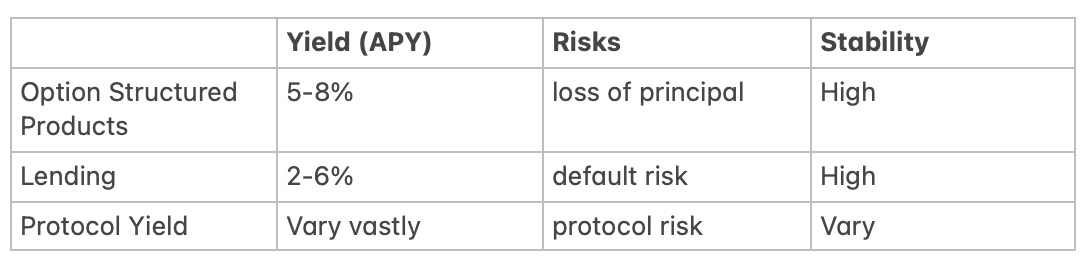

The Most Optimal Return on Risk for Real “Whales” to Generate Yield on BTC with Peace of Mind: Earlier this year, I was preparing a meeting with a sovereign fund with massive BTC holdings. A thought came to mind—if he asked me my recommendation to generate yield on their 9-figure BTC holding, what are even the options out there and who would I be comfortable vouching for? A couple came to mind:

Options/Structured Products Yield: The risk is the potential to lose some principal.

Lending Yield: Principal protected, but there’s counterparty risk—and many still have the scar tissue from FTX.

Protocol Yield: Perhaps the highest yield options with a wide spectrum of risks, mostly protocol-specific. Now let’s double-click to see the options:

STX: By far the longest-running protocol—founded in 2014 and token launched in 2018. It’s the earliest—and one of its kind protocol until the Bitcoin renaissance in 2023—to offer native Bitcoin yield natively for its stakers. Given the recent sBTC upgrade, the security of staking via STX is further graded by removing the need for a third-party custodian and now inherits 100% of Bitcoin security.

Arch Network, Babylon: Front-running solutions for protocol yields in the private market. Both enable native BTC yield generation with relatively low risks, but both are likely too new for conservative institutions’ risk appetite on their 9-figure holdings.

EVM Bitcoin L2s: Non-native and have major trust assumptions on the bridging solution, which are mostly via multisig. I’d be very hesitant to recommend protocol yield from EVM BTC L2s to someone like a sovereign fund.

The Undisputed Forerunner in Bitcoin L2 with 10 Years of First-Mover Advantage: Stacks has 10+ years of first-mover advantage over other new BTC L2s arising mostly between 2022-2023. STX is one of three BTC L2s that I can say with 100% certainty is not going anywhere.

A Rare Token Standard Moat: as detailed in this X thread, one of the only true moats of any ecosystem (L1 or L2) is its own token standard. And it’s harder than most think to build an ecosystem of startups using your token standard. This is why STX’s first-mover advantage and their own SIP 10 token standard will pay long-term dividends—this moat is very hard and takes very long to build, but once it’s there, liquidity and projects stay in your ecosystem. In the duopoly of EVM and SPL token standards as the two dominant threads, STX still managed to have 155 monthly active developers and 26 projects with live token built, and likely 60+ pre-launch startups building on top—that is no small feat

STX is Already an Ecosystem: Building an ecosystem—aka persuading founders to adopt your token standard (vs. using EVM or SPL)—takes Herculean efforts to achieve. In fact, this is why most new L1 and L2s are heavily subsidizing incubator/grant programs to attract builders.

Benchmarking & Comparables: As the dominant and largest Bitcoin L2 on the liquid market, STX is at ~$3.7B FDV (Fully Diluted Valuation) compared to more recent Ethereum L2s/app chains: Celestia $9B, Optimism $11B FDV, Arbitrum $11B FDV. Don’t forget, BTC market cap is more than 5x that of ETH. I wrote about my—relatively conservative—prediction and rationale for STX to be a $50B project here.

Token Maturity: STX’s circulating market cap/FDV ratio is 100% based on CoinGecko, fully vested, meaning there will be very limited sell pressure from unlocking/vesting. Personally, I’ve always stayed cautious of new tokens for long-term holding because of the sell pressure. 100% vested means that STX tokenomics has reached maturity—Solana is also about 81%, contrasted with other newer chains such as Arbitrum (~41%), Optimism (~29%), and Celestia (~41%).

Upcoming ecosystem catalysts:

Officially becoming a Bitcoin L2 via the Nakamoto upgrade (complete): STX now inherit 100% of BTC finality.

sBTC (mainnet on 12/16)

WASM ClarityVM, opening the doors to other languages like Rust, Solidity, etc., directly at the Stacks L2 level.

L1 integration: bring BTC to other L1s like Aptos network via sBTC

Good post!